The age-old question: To fix or not to fix?

28 May, 2019 / In Finance / By Chris Burnett

By Chris Burnett

When our clients are about to buy a house or looking at refinancing they often ask “should I fix my home loan?”. Unfortunately, without the luxury of a crystal ball it’s difficult to provide clients with the exact answer they are seeking as no one can predict the future and what will happen with interest rates overtime.

We can however, work through each client’s specific scenario with them and explain the various options available to them and the pros and cons of each option so that they can make an informed decision that is right for them.

What is the difference between a fixed home loan and a variable home loan?

Fixed home loans have an interest rate that is fixed for a set period of time – often between 1 and 5 years. At the end of the period the interest rate will convert to the standard variable rate set by the lender. The interest rate in a variable home loan will fluctuate over time – going up and down at any time. The changes in the variable interest rate will depend on factors such as the Reserve Bank cash rate, changes in market conditions or business decisions by the financial institution.

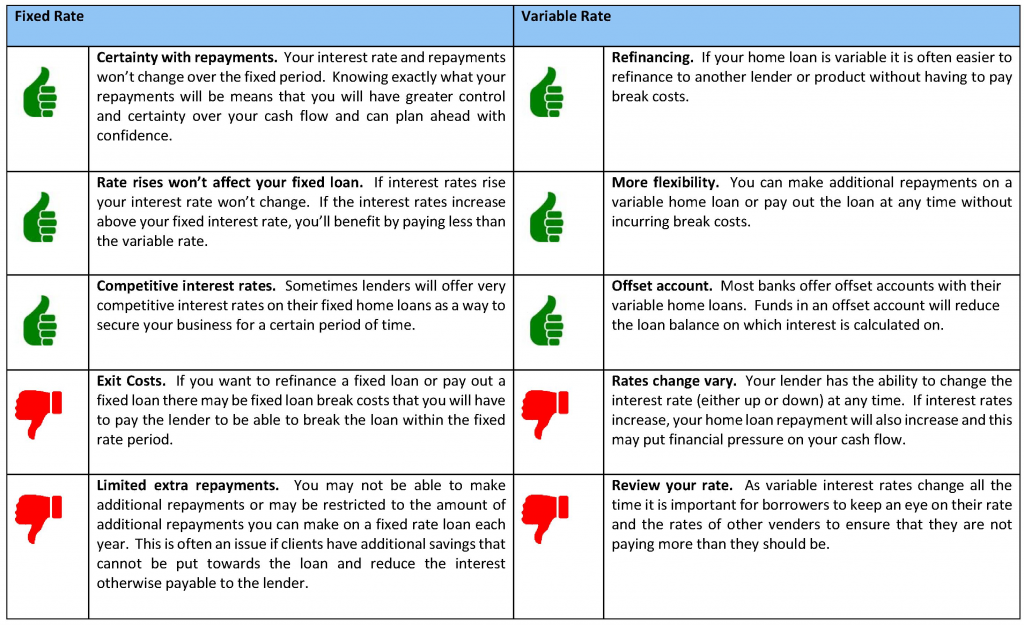

Pros and Cons?

There are pros and cons to both options of loans and it really depends on your individual circumstances and what you want from a home loan. There is often a trade-off between the flexibility of a variable home loan and the certainty of a fixed home loan. The table below shows some of the major pros and cons between the options.

The split approach: consider the best of both worlds.

Sometimes clients prefer the split approach where they will split their loan into two custom portions; one fixed and one variable. Taking this approach will give them some certainty over repayments on the fixed portion but still provide them with some flexibility over the variable portion – giving them the best of both worlds.

Final Comments

Everyone’s circumstances are different so there’s never going to be a one size fits all approach. Hence, the information provided here is general in nature only and does not constitute advice. It is recommended that you consult with us directly so that we can help determine what is best for you based on your specific situation, future plans and goals. Get in touch with us today for a review of your home loan facilities.